Manufacturing Startup Fast-Fund Finder

Your Current Situation

Why this works for you

Select your situation above to see the analysis.

Est. Time to Cash

Cost Factor

Watch out: Generic warning text

Fill out the details on the left to instantly match your manufacturing needs with the fastest funding options available in 2026.

You need cash, and you need it fast. When you are staring down a manufacturing line that isn't moving because of budget gaps, standard advice feels useless. In the world of Manufacturing Startup Fundingcapital specifically allocated for setting up production lines, equipment purchase, and operational costs in early-stage factories, time is the enemy. You cannot wait six months for a traditional commercial loan approval when your rent is due next week.

The Reality of "Right Now" Funding

First, let's get one thing straight: legitimate institutions do not hand over large sums of cash instantly upon request. If someone promises instant millions without checks, run. However, there are faster channels than the average three-month bank application process. To get money quickly, you usually trade speed for cost or equity.

In 2026, digital banking has tightened security but sped up verification. Some fintech lenders offer decisions within 24 hours, but approval depends entirely on your past data flow. If you are a brand new startup with no history, your personal assets become the primary collateral. Here are the actual pathways available to you today.

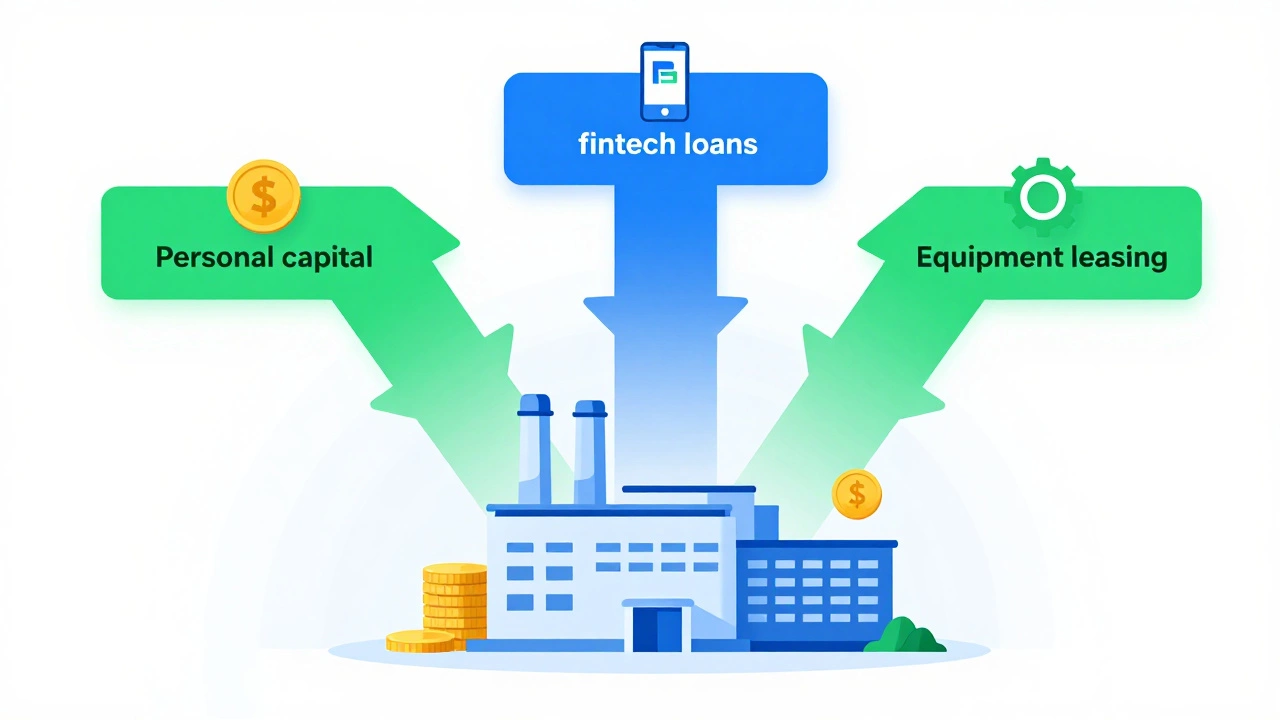

1. Personal Capital and Friends/Family

This is often overlooked because it feels uncomfortable. Yet, it remains the fastest method globally for early-stage capital. Using Personal Savingsexisting liquid assets belonging to the founder used to finance initial business operations bypasses the entire approval cycle. You own the money, so you deploy it immediately.

- Pros: Zero interest rate, no credit checks, complete control.

- Cons: Risky to your personal financial security, potential relationship strain if things go wrong.

If you reach out to friends or family, draw up a formal agreement even if they say no paperwork is needed. Define repayment terms clearly. Treat this as a real transaction to preserve relationships and maintain professionalism.

2. Fintech and Online Lenders

Traditional banks like HSBC or Barclays can take weeks. Small Business Loansdebt facilities offered by financial institutions specifically designed for SMEs to bridge cash flow gaps from online platforms move much faster. Companies offering merchant cash advances or working capital loans can disburse funds in under 48 hours once documentation is uploaded.

These services analyze your current bank statements via open banking APIs. If you have sales history showing consistent revenue, they view you as lower risk. For a manufacturing unit, they might look at your purchase orders. If a major retailer has pre-ordered your goods, some lenders will front you the capital to fulfill the order based on that contract.

3. Equipment Financing and Leasing

Do not spend all your cash on machines. Instead, borrow against the machinery itself. Equipment Leasingan arrangement where a third party purchases manufacturing equipment and rents it to the business owner allows you to keep cash in your pocket for raw materials.

Most leasing companies know their asset values well. Because the machine serves as collateral, approval is often quicker than unsecured loans. You walk away with the tools to produce without paying the full upfront cost. In many jurisdictions, these leases are also tax-deductible expenses.

| Source Type | Typical Approval Time | Interest/Risk Level | Collateral Needed |

|---|---|---|---|

| Personal Savings | Instant | None | None |

| Fintech Loan | 1-3 Days | High Interest | Credit Score/Guarantor |

| Equipment Lease | 3-5 Days | Moderate | The Equipment Itself |

| Govt Grant | 30+ Days | No Repayment | Biz Plan/Impact Proof |

| Angel Investor | Weeks to Months | Equity Loss | Growth Potential |

4. Government and Local Council Schemes

I live in Liverpool, and here the council offers various regeneration schemes. While waiting for government help takes longer, it provides free capital you don't repay. Look for programs tied to regional development or innovation. In 2026, green technology incentives are massive.

If your manufacturing process involves recycling materials or uses energy-efficient machinery, Government Grantsnon-repayable funds distributed by state bodies to support specific economic goals become a viable option. These require detailed applications and rigorous reporting, but they are worth the effort for long-term stability. Check local industry associations; they often act as intermediaries to simplify the bureaucracy.

5. Invoice Factoring

Have you delivered goods but not received payment yet? You are holding onto money stuck in your client's account. Invoice Factoringa financial service where a business sells its unpaid invoices to a third party for immediate cash solves this liquidity trap.

A factoring company buys your outstanding invoices at a discount. They advance you 80% to 90% of the value immediately. Once the client pays the invoice, they release the rest minus a fee. This converts your accounts receivable into immediate working capital. This is particularly useful for B2B manufacturers who deal with 60-day payment terms.

6. Equity Investors

Selling ownership stakes is another route. Angel Investorsaffluent individuals who provide capital to startups in exchange for equity ownership are wealthy people who bet on your success. Unlike banks, they want to see growth, just repayment.

This is not usually an overnight fix. You need to pitch your deck, due diligence happens, and contracts take weeks. However, once signed, the transfer of funds is relatively quick compared to public markets. For a manufacturing idea with high scalability, this might be your best bet for larger sums.

Preparing Your Documents for Speed

To shorten approval times, have these documents ready before applying anywhere:

- Business Plan: One-page executive summary explaining exactly how you spend the money.

- Financial Projections: Realistic cash flow forecasts for the next 12 months.

- Proof of Orders: Signed contracts showing future demand for your products.

- Bank Statements: Last six months of personal and business accounts.

Lenders hesitate when information is missing. A clean, organized file shows competence. It signals that you manage details well, which reduces their perceived risk.

What to Avoid

Beware of any entity promising "guaranteed approval." Legitimate investors evaluate risk; guarantees imply they don't care. Watch out for predatory lenders charging astronomical APRs that will bankrupt you before production starts.

Never sign a "blank check" or power of attorney. Protect your personal assets wherever possible. If you are struggling financially, seek free advice from organizations dedicated to small business support rather than taking the first loan offered online.

Strategic Next Steps

Money alone won't save a bad business model. Before you even sign for funds, ensure your unit economics work. Calculate the cost per unit accurately. Factor in waste, electricity, labor, and overheads.

Start with low-cost methods. Bootstrap using personal savings or pre-sales. Use customer deposits to fund production. Only turn to debt or equity once you have proven traction. This approach keeps you solvent and in control while you build the factory floor.

Can I get a loan without checking my credit score?

It is very difficult. Most financial institutions require a credit check to assess risk. However, secured loans backed by assets like equipment or property might ignore poor credit history more easily.

How fast can a manufacturing grant be approved?

Government grants typically take between 30 to 90 days to process. While slower, they do not require repayment, making them valuable for non-urgent expansion projects.

Is invoice factoring safe for startups?

Yes, it is generally safe if your customers are creditworthy. Since the factor collects directly from your clients, it helps your cash flow without increasing your debt ratio.

Should I use personal savings for my factory?

It is common for founders to bootstrap initially. Just ensure you keep enough personal emergency funds for living expenses to avoid putting yourself in a crisis situation if the business struggles.

Are crowdfunding options viable for hardware startups?

Crowdfunding works best for consumer-facing products. If your manufacturing output targets B2B wholesale, it is harder to sell shares to the public. Equity crowdfunding exists but requires regulatory compliance.